When is refinancing worth it? How much should your rate drop?

Erik J. MartinThe Mortgage Reports Contributor

April 14, 2022 - 12 min read

Is refinancing worth it right now?

Refinancing is usually worth it if you can lower your interest rate enough to save money month-to-month and in the long term. Depending on your current loan, dropping your rate by 1%, 0.5%, or even 0.25% could be enough to make refinancing worth it.

This means that even in a rising-rate environment, a refinance is still worthwhile for some homeowners.

If you think you could get even a slightly lower rate, check to see if a refinance is worth it based on your new rate and savings.

Is it worth refinancing for 1 percent?

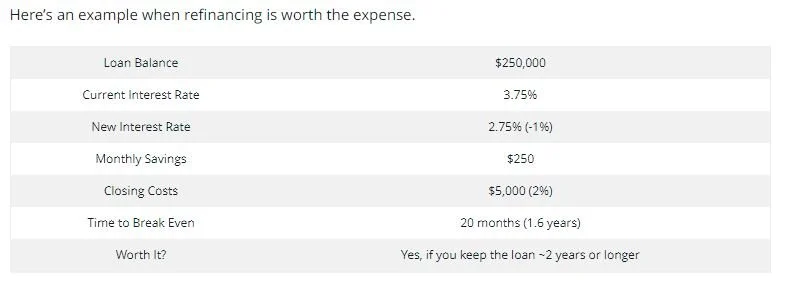

As a rule of thumb refinancing to save one percent is often worth it. One percentage point is a significant rate drop, and it should generate meaningful monthly savings in most cases.

For example, dropping your rate a percent — from 3.75% to 2.75% — could save you $250 per month on a $250,000 loan. That’s nearly a 20% reduction in your monthly mortgage payment.

Those monthly savings can be put toward daily living expenses, emergency funds, investments, or paid back into your mortgage to pay the loan off early and save you even more money in interest.

Refinancing for a 1 percent lower rate

Here’s an example when refinancing is worth the expense.

Keep in mind, “breaking even” with your closing costs isn’t the only way to determine if a refinance is worth it.

A homeowner who plans to move or refinance again before the break-even point might opt for either:

A no-closing-cost refinance

Rolling closing costs into the refinance loan

1. No-closing-cost refinancing

A no-closing-cost refi typically means the lender covers part or all of your closing costs, and you pay a slightly higher interest rate in exchange.

Accepting this higher rate will eat into your monthly savings. But if you’re still saving enough when compared to your existing mortgage loan, this strategy can still pay off.

You’d be avoiding closing costs and still saving money month to month, so you wouldn’t have a break-even point to worry about.

This is often a win-win situation for borrowers who plan to keep their new loan for only a few years.

2. Rolling the closing costs in your new loan

Rolling closing costs into the refinance loan will increase your principal balance and total interest paid. But if you’re going to keep the loan for more than a few years, rolling closing costs into the loan amount may be more affordable than accepting a no-closing-cost loan with a higher interest rate.

“Most borrowers choose the latter— lumping the closing costs into the loan so they can receive the lowest possible rate. But that’s not always the best option unless you plan to stay in your home for at least several years,” says says Tom Furey, co-founder of Neat Capital.

Is it worth refinancing for 0.5 percent?

There are two common scenarios when refinancing for half a percent could be worth it:

If you’ll keep the new loan long enough to recoup closing costs (breaking even)

OR, if you can get the lender to cover your closing costs with a no-cost refinance loan (“Double check that costs aren’t actually being rolled into the loan,” cautions Jon Meyer, The Mortgage Reports loan expert and licensed MLO)

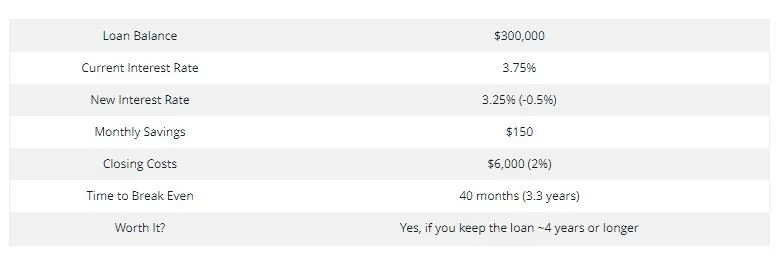

1. Refinancing for 0.5 percent: Break-even method

First, let’s look at a break-even scenario.

Remember, the less your rate drops, the less you save each month. So it takes longer to recoup your closing costs and start seeing “real” benefits.

For example, dropping your rate 0.5% — from 3.75% to 3.25% — could save you about $150 per month on a $300,000 mortgage loan.

That’s a decent monthly savings, but it will likely take you over three years to break even with closing costs. So you want to be sure you’ll keep the refinanced loan for at least that long.

Now let’s look at how the numbers compare if you can drop your mortgage interest rate by 0.5% using a no-closing-cost refinance.

2. Refinancing for 0.5 percent: no-closing-cost method

Say your current mortgage rate is 3.75%. Your refinance lender offers you a new rate of 2.5%.

Instead of accepting the ultra-low rate, you ask the lender to pay your closing costs. The lender agrees, and in exchange, you accept a higher rate than the initial offer: 3.25%

This arrangement only lowers your interest rate by 0.5%. But there’s no break-even point because you paid no upfront closing costs. So you start seeing “real savings” from your lower monthly payment right away

“A thing to note here: While this isn’t true of all loan officers, most tend to quote ‘no cost refis’ as often as possible. So if you can save 0.5% in this case, it’s a great deal,” adds Meyer.

Of course, you would save a lot more money both month-to-month and in the long run if you accepted the lower mortgage rate and paid closing costs upfront.

Those who can easily pay the closing costs out of pocket should typically do so.

But for homeowners without a lot of savings, it might make sense to accept the higher, no-cost rate. This could allow you to refinance and see month-to-month savings without having to worry about the initial cost barrier.

Is it worth refinancing for just 0.25 percent?

As a rule of thumb, experts often say refinancing isn’t worth it unless you drop your interest rate by at least 0.5% to 1%. But that may not be true for everyone.

Refinancing for a 0.25% lower rate could be worth it if:

You are switching from an adjustable-rate mortgage to a fixed-rate mortgage

You have a large loan balance

You can refinance to consolidate high-interest debts

You are leveraging home equity with a cash-out refinance

You have a jumbo loan with significantly higher interest rates

1. Refinancing into a fixed-rate loan

“Say you are refinancing from an adjustable rate to a 0.25% lower fixed rate. Here, refinancing may make sense. That’s especially true if you expect interest rates to increase,” says Bruce Ailion, Realtor and property attorney.

2. Refinancing a large loan amount

A quarter-point rate drop may also benefit someone with a large principal borrowed.

“A large loan size may result in significant monthly savings for a borrower, even when rates dip by only 0.25%,” says David Reischer, attorney and CEO of LegalAdvice.com.

To illustrate this point, consider the following example from Steven Ho, senior loan officer at Quontic Bank:

Assume you have a $500,000 mortgage at a 4.5% rate

Your monthly principal and interest payment is $2,533, with a PMI payment of $250

So your total monthly payment is $2,783

You opt to refinance to a 4.25% rate (0.25% lower than your initial rate)

This would reduce your monthly payment to $2,459 — saving you $324 per month

“Over five years, that adds up to over $19,000 in savings,” Ho notes.

Even if you pay 2% in closing costs on that $500,000 loan, your upfront cost is just $10,000. So you save almost twice as much as you spent on the refinance within the first five years.

3. Refinancing to consolidate debt

Refinancing for 0.25% might also make sense in the case of a debt consolidation refinance.

“Imagine you have $20,000 in credit card debt. The interest on this credit card is 25%, which adds up to paying $416 a month just in interest,” Ho says.

Say your original mortgage balance was $500,000 at a 4.5% fixed rate, equating to a $2,533 monthly mortgage payment. But you decide to roll your $20,000 in credit card debt into your mortgage refi.

You’ll now have a $520,000 mortgage balance and a higher monthly payment of $2,558 after refinancing to a 4.25% rate.

“Your mortgage payments go up $28 extra a month. But your overall savings would be $391 a month. That’s because you’re no longer paying 25% interest on the credit card debt,” adds Ho.

4. Cash-out refinance and home improvement loans

Say you plan to take cash out during your refinance. Then, the decision to lower your rate by 0.25% via a refi gets more complicated.

“With a cash-out refi, your monthly mortgage payment may not go down,” says Reischer.

“But you can use the cash taken out to consolidate other higher paying debt obligations. Or it can be used to make needed home improvements. That can be a very good reason to do a cash-out refi — to make upgrades that will increase the value of your property.”

Also, think about refinancing to a shorter mortgage term — like from a 30-year mortgage to a 15-year loan with a fixed rate.

“This can yield even lower refinance rates. And it can result in you paying less in interest payments over the life of your loan,” says Ailion.

When is it worth it to refinance?

It’s generally worth it to refinance if you can lower your costs in some way, whether by getting a lower interest rate, a shorter loan term, or a cheaper monthly payment.

A lower interest rate means you’ll have lower monthly payments compared to your existing mortgage. And it often means you’ll save thousands (maybe tens of thousands) over the life of the loan.

But you have to weigh those savings against the inherent downsides of mortgage refinancing:

You have to pay refinance closing costs on the new mortgage, which are typically 2%-5% of the new loan amount. These include origination and application fees, along with legal and appraisal fees

You restart your loan term from the beginning, usually for another 30 or 15 years

If your new interest rate isn’t low enough, you might actually pay more interest in the long run because you pay it for a longer time

Plus, most people don’t stay in their homes long enough to pay their mortgages off. So you should make sure the savings you calculate are realistic. Account for the amount of time you plan to keep your mortgage and the upfront cost of refinancing.

In short, the numbers in this article are only examples. You can use them as guidance, but make sure your refinance decision is based on your own loan details and financial goals.

“Determining whether the total costs to refinance makes sense heavily depends on how long you plan to keep the loan,” says Furey.

“Assume your ultimate refinance goal is to save money. If so, you’ll want to determine that your long-term savings exceed the costs to secure the refinance.”

To estimate if a mortgage refinance is worth it for you, try this refinance calculator.

Other good reasons to refinance (besides a lower rate)

Most people who refinance their existing home loans want to save money by getting a lower monthly payment and a lower interest rate.

But there are other reasons to refinance. While your new mortgage should save you money, there are several ways a loan can do this — and they don’t always include a lower rate:

Refinance an adjustable-rate loan into a fixed-rate loan

Drop mortgage insurance premiums

Tap home equity

Shorten the loan term

1. Replace an ARM

Rates on adjustable-rate mortgages (ARMs) will eventually start fluctuating with the broader market each year. If you have an ARM, refinancing lets you lock in a fixed rate based on current market conditions and your credit profile.

Getting a fixed-rate mortgage can protect you from the possibility of paying a lot more interest later.

Even if you end up with a higher payment on your fixed-rate mortgage at first, the loan could pay off a lot later if interest rates increase.

2. Get rid of mortgage insurance

FHA and USDA loans charge ongoing mortgage insurance fees. Homeowners pay these fees — along with their monthly mortgage payments — to protect mortgage lenders from losing money if they default.

In many cases, FHA and USDA homeowners keep paying mortgage insurance for the life of the loan.

But you can eliminate these fees by refinancing into a conventional loan which may not require mortgage insurance coverage. Conventional loans require private mortgage insurance (PMI), but only until the loan balance gets paid down to 80% of the original loan amount.

Even if you don’t shave much off your interest rate, getting out of FHA or USDA mortgage insurance could save you lots of money.

3. Cash out home equity

The difference between your home’s value and the amount due on your mortgage is your home equity.

A cash-out refinance lets you borrow this equity to use on debt consolidation, home improvements, or even a down payment on another property.

Ideally, you’ll also get a lower-rate loan when you do a cash-out-refi. But if you can’t lower your rate — or shorten your mortgage term — you might consider getting a home equity loan or a home equity line of credit instead of a cash-out refi.

4. Shorten your loan term

Time is one of the biggest factors affecting how much interest you’ll pay on a mortgage loan. Longer-term loans give mortgage lenders more time to collect interest on your debt. So you’ll pay more interest on a 30-year loan than on a shorter-term mortgage.

By shortening your loan term, you could save money over the life of the loan even if you don’t score a lower rate. Just keep in mind your monthly mortgage payments will increase because of the shorter term.

Verify your refinance eligibility. Start here (Jun 14th, 2022)

When is refinancing not worth it?

It’s important to remember that refinancing starts your loan term over. That means you’re spreading the remaining loan principal and interest repayment over a new 30-year or 15-year loan term.

This has big implications for the long-term cost of your new loan. As such, refinancing might not be worth it if:

You’ve been paying your original loan for quite some time

Refinancing results in higher overall interest costs

Your credit score is too loan to qualify for a lower rate

1. You have had your current mortgage for a long time

Homeowners who are a decade or more into their mortgages are less likely to see savings with a small rate decrease, because they’ll be extending the full payoff period to 40 years or more — and paying interest on all that ‘extra’ time.

One solution is refinancing into a shorter loan term — like a 20- ,15-, or 10-year mortgage — instead of beginning all over again with a new 30-year loan.

Shorter terms typically have lower rates. And you’ll likely save even more in interest because you pay off the loan sooner.

But keep in mind: The shorter your loan term is, the higher your monthly payments will be. So a shorter loan term is not always an affordable option.

“That said, if your original loan is, say, around $500,000 at 4%, and you’ve made 11 years of payments — you could refi into a 15-year term at 3% and only pay a couple hundred extra each month and shave 4 years of monthly payments off of your loan,” says Meyer.

In situations where a homeowner is nearly done paying off their home loan, a refinance rarely makes sense.

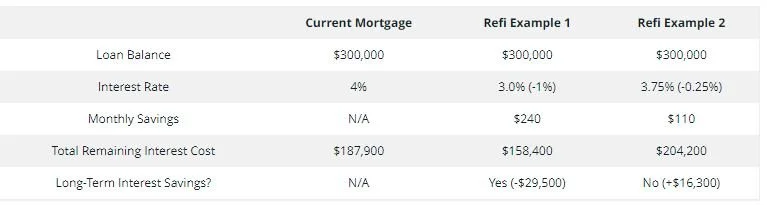

2. Refinancing would increase your total interest cost

If your new rate is not low enough to generate long-term savings, you could end up paying more interest over the full loan term.

Take a look at an example:

Both these refinance scenarios save the borrower money month-to-month. But only the first one — where they drop their rate 1% — yields long-term savings.

The second refinance option — dropping the rate by 0.5% — actually costs this borrower $16,000 more if they keep their loan its full term.

Of course, most homeowners do not keep their mortgage for its full term. And, according to data from Freddie Mac, the median number of years a home buyer will refinance their initial mortgage is 3.6 years.

This changes the math. Someone who’s only going to keep the refinanced loan for 3-5 years, for instance, will not pay nearly as much extra interest as someone keeping it the full 30.

The right decision also depends on your reason for refinancing.

For example, even the second refinance option might make sense if the homeowner has had an income reduction and needs to lower their mortgage payments to be able to afford them.

Maybe one spouse or partner became a stay-at-home parent or their job was eliminated during an economic downturn.

If they can get a no-cost refi and a 0.25% rate reduction, they might be happy with the $100 monthly savings on their new loan — despite a higher long-term cost.

3. Your credit score is too low to refinance or get a good rate

This may not be a great time to refinance if you have a low credit score and can’t qualify for a competitive mortgage interest rate.

Mortgage lenders tend to give the best mortgage refinance rates to applicants who have the strongest credit profiles.

You won’t need perfect credit to get a good refinance rate. In fact, it’s possible to get an FHA refinance with a credit score as low as 580. But many lenders require scores of 620 or higher.

When you can’t qualify for an interest rate that’s lower than your current loan’s rate, consider improving your credit score before applying.

Or, ask a lender about Streamline refinancing if you have an FHA-, USDA-, or VA-backed loan. With a Streamline Refinance, you could potentially get a new mortgage without a credit score check.

Today’s refinance rates

The bottom line? It’s a good time to refinance when your savings are greater than the cost.

“If refinance rates are declining, it may pay to wait to maximize the difference between your current rate and the new rate,” Ailion adds. “But when lower refinance rates begin to rise, it’s probably a good idea to pull the trigger.”

Today’s mortgage rates are still relatively low, but they may not be around forever. It’s a good time to consider locking in a low refinance rate to maximize your savings.

Experiment with a mortgage calculator to see when the numbers make sense for your financial situation. Or simply begin getting quotes from multiple lenders below.